Ninety-four Indians were added to the Hurun global billionaires’ list that came out Tuesday, March 27, the highest from any country other than the United States. A record run in the stock markets, profit margins at a 10-year high and robust credit growth along with a deflationary wholesale price index (WPI) have left India Inc. ecstatic. But the euphoria might not last, and the signs are showing.

Why India Inc. May See Profit Margins Slim Next Financial Year

Notwithstanding weak sales growth, companies managed to hold on to their profit margins because of lower costs. But with WPI back in the inflation zone and no big boost to sales in sight, delivering strong margins growth may not be easy

Pressure on margins

Advertisement

As the new financial year begins, Indian companies must face a humbling reality: they have not managed strong revenue growth all through FY2024. An Outlook Business analysis of Nifty 500 companies showed that while most companies posted big profit margins, underlying revenue growth remained weak.

Getting Lucky

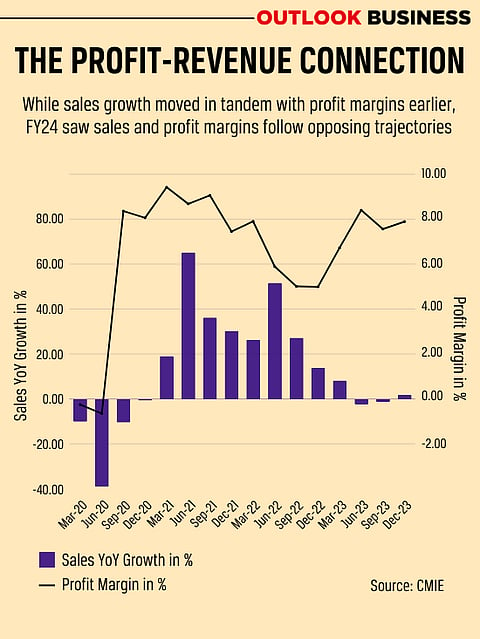

In 2021–2022, Indian companies saw a net sales growth of 39 per cent. The growth in sales came despite an inflationary environment when WPI inflation remained in double digits in all quarters between April 2021 and September 2022. A strong growth in sales allowed companies to offset rising costs. Net profit margins were at 8.27 per cent.

The next fiscal year, FY23, this growth slowed to 25 per cent. The average profit margin came down to 5.6 per cent for the Nifty 500 companies.

In the 2024 financial year, there was a steep fall in net sales growth, with the first two quarters reporting negative sales growth of 2.26 per cent and 1.14 per cent, and the third quarter showing a growth of a measly 2 per cent, according to data sourced from Centre for Monitoring Indian Economy (CMIE).

Advertisement

Even as sales growth dipped, profit margins widened. The average net profit margin for the non-financial sector in the first three quarters stood at 7.95 per cent.

Revenue stayed low, but companies had no trouble maintaining consistent profit margins. This was made possible by a decline in input costs.

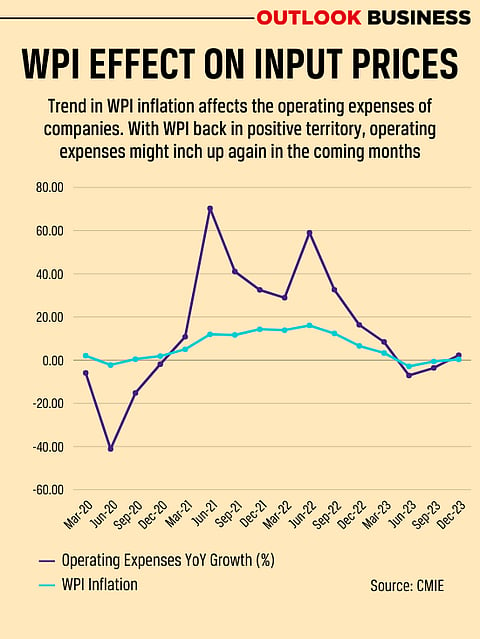

Between April and October 2023, WPI inflation slipped into the negative. Tepid demand started hurting the topline of company balance sheets, but the bottomline kept up as pressure on operating expenses eased. Operating expenses declined in two out of three quarters in the 2024 financial year.

The Trouble with Good Luck

But now, WPI inflation has stayed positive for four months in a row. Raw material costs are rising and the time to tolerate sluggish revenue growth is running out. Margin expansion seen in the last few years will be difficult to continue as the operating environment changes, according to an analysis of BSE500 firms by DSP Asset Managers, a Mumbai-based asset management company.

Advertisement

“Subdued WPI inflation levels over the last several quarters helped EBITDA [earnings before interest, taxes, depreciation and amortization] margins recover from higher inflationary pressure of 2022 and early 2023. However, the margin expansion tailwinds appear to have run their course. Earnings growth of between 18 per cent and 25 per cent over the last three years would be hard to repeat for the broader set of firms,” the analysts said in a research note published in March.

What compounds the problem for companies is that there are no signs of a robust recovery in private final consumption expenditure (PFCE), an indicator of demand. PFCE growth is pegged at 4.4%, the lowest in 20 years except the pandemic year, according to government estimates.

Weak monsoon has hurt agriculture. Real rural wage growth is at 0.5%, according to Gaura Sengupta, Economist at IDFC First Bank. Wage growth in urban areas has also seen a considerable slowdown, as per the analysis of DSP Asset Managers. Coupled with these, high retail inflation has put a damper on demand.

Advertisement

“We could see some moderation in urban demand in FY25 with companies profit growth expected to slow as support from lower input costs wanes,” says Sengupta.

A sustained slowdown in urban demand along with low momentum in rural areas may put Indian companies in a fix. But analysts say it is too early to panic and how the next financial year pans out will only show after the elections are over.

The dominant theme for companies is going to be consistent revenue growth, says Ambareesh Baliga, an independent market analyst. “It is a must for companies if they want to hold on to their good margins. But not much is expected to happen till the elections conclude in June.”

With the final earnings season for financial 2024 to kick off in April, observers will be keenly watching the revenue growth trajectory. Meanwhile, India Inc. will go into financial year 2025 with focus on recovering the lost momentum in the topline of their balance sheet.

Advertisement