India in its mind maybe winning the race of net zero, but the public-sector undertakings (PSU) of its energy sector would have a different take on the matter altogether. Moving to cleaner energy models is not supposed to be an overnight process and requires some heavy lifting, especially in case of a country that majorly relies on old infrastructure. And if the company does not upgrade the infrastructure, it invites scrutiny from investors on environmental, social and governance (ESG) grounds, which can potentially remove it out from the competition. Unfortunately, many PSUs in India today fear the possibility of this.

Energy Transition: Indian Maharatnas' Push For Renewables Hits A Funding Roadblock

PSUs in the country are struggling to catch pace with their private peers in India's energy transition into the renewable space. Hence, a fear of scrutiny has arise for these state-owned companies from the investor front

Green financing still remains a challenge for PSUs in India

Advertisement

Union Power and New & Renewable Energy Minister RK Singh in September assured that India will comfortably achieve its 500 GW renewable energy target before the 2030 deadline. He then went on to lay emphasis on India’s lower per capita emissions at 2.2 tonnes, compared to the global average of 6.3 tonnes. Furthermore, the minister said India is the only major global economy whose energy transition actions are aligned with limiting the global temperature rise to less than two degrees Celsius. These claims would suggest to anyone that India is very well on its path to achieve its net zero emissions target by 2070. However, like India’s energy transition actions, the policies of the country do not seem similarly aligned to ensure equal participation from the PSU side and save them from scrutiny.

India’s ongoing transition to clean energy is heavily backed by big private names like Adani and Greenko, among others. As a result, India’s energy transition story comes as private-led with state-owned entities struggling to catch pace. What places the PSUs behind in the race is the lack of motivation among investors to support the financing of renewable energy projects. Experts view this as a significant flaw in government’s transition plan, which if not fixed can ultimately doom the PSUs in the renewable space, be it Navratna or Maharatna.

Advertisement

“An energy transition will inevitably be a technology transition to reduce emissions, and the cleaner technology spectrum offers a range of near-term, medium-term and long-term solutions. These cleaner technologies will need financing and policy support to reach giga-scale,” says Gauri Jauhar, Executive Director at S&P Global Commodity Insights.

According to a report by the International Institute for Sustainable Development (IISD) and the Council on Energy, Environment and Water (CEEW), total investment by India’s seven energy related Maharatnas into renewable energy excluding hydro aggregated to just Rs 25,000 crore between FY14 and FY20. The investment was said to be 10 times lesser than their investments in fossil fuel. “The private sector leads in the 55 GW of capacity that is scheduled for completion in the next 2-3 years based on developing the capabilities to complete in tenders, set-up and operate the plants,” said Jauhar.

In the last three financial years, one of India’s leading energy Maharatna, NTPC Ltd added 1,854 MW capacity into its renewable energy portfolio, which is significantly lower than Adani Green Energy’s (AGEL) addition of 4,841 MW. Under government’s push, NTPC has announced an investment worth of Rs 2.5 lakh crore in its 2030 plan to create capacity of 60 GW. However, the company that has an installed capacity of 3.4 GW would require extensive financing to match up with AGEL and Greenko, who already have a current capacity of 8.4 GW and 7.5 GW, respectively.

Advertisement

No Love for the Green

Indian PSUs’ struggle to raise funds for these projects can be best observed in the underdeveloped green bond market in the country. According to a report by Fitch Ratings, India requires more than $10 trillion in green funds to meet its goals. However, the green bonds at the beginning of this year accounted for a mere 3.8 per cent of the overall corporate bond market in India. The domestic debt market is usually the prime source of raising funds for many PSUs but has failed them in their ESG endeavors due to the lack of government support. This thematic market, which was developed first by the World Bank in 2008, is helping many countries globally but not India.

As per the data sourced from Climate Bonds Initiative, the global market for sustainable finance is growing rapidly on back of green bond issuances, which surpassed the $2 trillion mark last year. Of this, green bonds aggregating $230.9 billion were issued by 26 sovereigns with European nations being the major issuers. Indian government, on the other hand, has only this year joined the market by raising Rs 160 billion through these bonds.

Advertisement

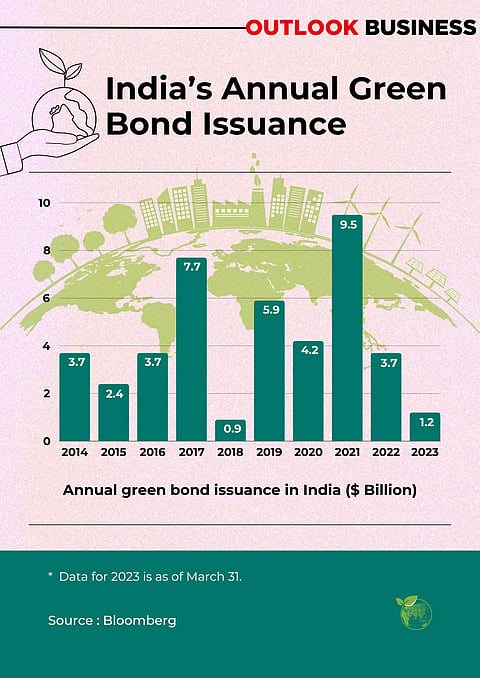

India's Green Bond issuance

Companies in India, according to a Bloomberg report, have only managed to raise $43 billion through green bonds since 2014. “At the moment, the markets in India are not supportive for PSUs to transition into the renewable energy space. Currently there is no benefit for the investors to support the financing of renewable energy projects which is making it difficult for the PSUs to raise funds. Private players can do it because they offer higher price for higher risk of course,” says a senior PSU official requesting anonymity.

Due to the green bonds in India having no tax benefits, subsidies or any special scheme, unlike western countries, investors have absolutely no reason to divert their money into these bonds. REC, a state-owned NBFC and a frequent issuer in the corporate bond market, for its plan to raise funds to finance eligible green projects in India chose to turn offshore this year when it raised $750 million through dollar-denominated green bonds. The company carried out investor road shows spanning two weeks in countries such as the US and the UK to make the issue successful.

Advertisement

Back home, National Bank for Agriculture and Rural Development (NABARD) came up with India’s maiden social-sector bond offering in September, where it had planned to raise up to Rs 30 billion but could only get Rs 10.4 billion through the issue. The reason for the company not been able to raise even half the amount was cited as the difference between the price quoted by the issuer and the investors, by a company official. “If NABARD couldn’t get the investors on board then it is unfair to even think that any other PSU would be able to fetch investors’ interest without the government’s intervention,” said the PSU official quoted above.

Typically, bonds issued by NABARD are considered the benchmark in the corporate bond market, which has always been dominated by PSUs. The performance of its bonds is considered crucial for any state-owned issuer planning a debt offering.

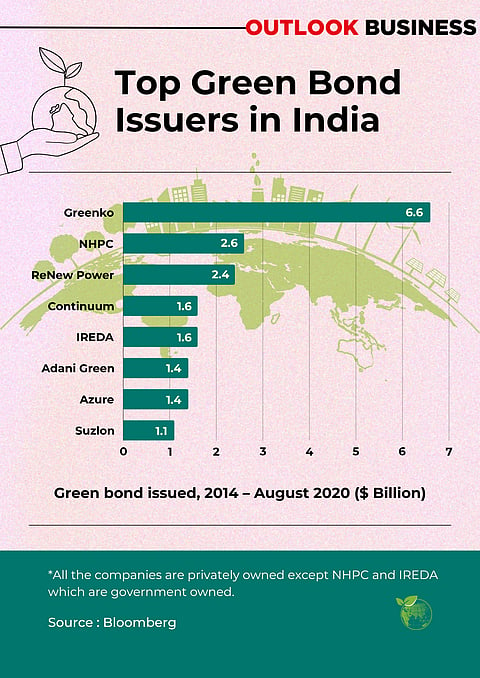

Green Bond issuance by companies

Scrutiny Awaits

Today, many energy PSUs such as NTPC, NHPC and NLC, among others, are foraying into the renewable energy space. While the debt market route is currently not lucrative for them, these companies are naturally left with the option of bank loans to raise capital. Since the bond market has always been a more viable option for the PSUs to raise funds at cheaper rates due to their state-owned tag, bank borrowings will likely increase their expenditure as the time goes. NTPC Renewables Ltd, incorporated in 2020, recorded a loss of Rs 137 lakh for the year 2022-23 and is nowhere in a place to compete with a private player like Adani Green Energy which had a profit of Rs 973 crore in the same period.

The gap between the private sector and the public sector in the current time will suggest that it is impossible for the PSUs to catch up with their private counterparts in the transition to renewable energy. However, the major issue remains the access of capital that bridges this gap further. Most of the reputed global financial institutions, funds, investors and lenders have their own ESG requirements that need to be fulfilled and therefore have developed their own ESG frameworks aligned with IFC Performance Standards. While the PSUs are trying to develop their portfolios to win the confidence of stakeholders, limited access to capital puts them out of the game.

“A number of private companies in the renewable energy space have been funded through institutional capital that demands adoption of ESG frameworks as per IFC Performance Standards. For such private companies, ESG risk mitigation and disclosure becomes an intrinsic factor to secure the capital,” says Manikkan S, Executive Director and CEO of Radiance Renewable. The IFC Performance Standards are designed to help companies manage the environmental and social risks associated with their projects, and to ensure that these risks are mitigated.

Since India’s independence, PSUs have played a vital role for the Indian economy. Even today, over 50 per cent of the power generated in the country is by these companies. However, as the world moves towards a new future that is renewable energy, they grapple with the challenge of traditional and outdated infrastructure. Where the private players, who adapted sustainability long ago, are better placed to raise funds due to their robust ESG frameworks and higher interest rates offered, the place of energy PSUs in the renewable future hangs in balance.