Research by Refinitiv found that almost three-quarters of the quant community said COVID-19 had harmed their models, with more than one in ten saying that the pandemic had made their models obsolete. What caused these problems and how can quants adapt to the new environment?

Quant Factors: The Hype. The Hole. The Hope

Quant funds’ computer models rely on finding patterns in historical data

Quant Factors: The Hype. The Hole. The Hope

Advertisement

- Quants struggled in 2020, but the underperformance gap has narrowed in 2021.

- Size, value and momentum are important in quant research, but quants can neglect to create models responsive to real-world shocks.

- As the quant community continues to recover in 2021, adaptive data inputs and algorithms need to be top of mind.

Quant funds’ computer models rely on finding patterns in historical data, and very few could successfully trade through 2020’s once-in-a-century pandemic. There has been some narrowing of the underperformance gap in 2021, but the crux of the issue remains – most quants need to update.

The quants that thrived in 2020 have adaptive data and models. As concerns about COVID-19 spread through the investment media, models based on media sentiment were able to quickly re-balance.

Advertisement

Why did COVID-19 cause problems for the quant community?

Academic and industry research has long identified that share prices move in patterns in response to information flow, called overreaction (mean-reversion) and underreaction (trending).

Data based on such events helps quants identify breaking events – even anomalous events such as COVID-19 – by extracting the most predictive interpretations from the market’s reactions. Despite this awareness, many quants have been slow to adopt such insights.

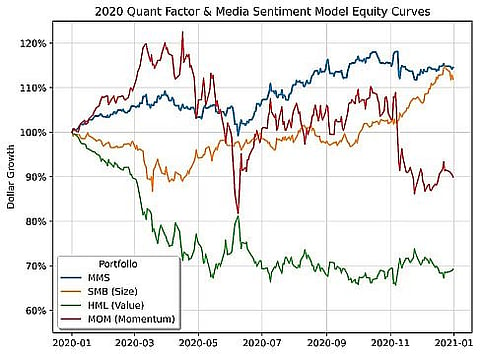

Figure 1 below compares the performance of a quant factor built from media sentiments and themes (MMS) with traditional factors Size (SMB), Value (HML), and price momentum (MOM) from January 2020 through to April 2021.

Figure

A plot of the performance of the most common quant factors (the 3 Fama-French factors) and the MMS after its launch in Jan 2020, from Jan 2020 through Apr 2021. Source: Refinitiv MarketPsych Media Sentiment Model.

Size, value, and momentum, the three of the major investment “factors” that economists have discovered, tend to lead to above-average returns in the long run. They involve grouping stocks according to a defining characteristic, such as their size, their cheapness, or their price change.

Advertisement

Systematically mining such factors is the heart of the hype around the computer-powered, algorithm-driven quantitative investment industry. But in the rush to find factors that worked historically, quants often forgot the importance of creating models responsive to real-world shocks and regime changes, and this neglect led to significant quant underperformance.