Earlier, they were not compelled to generate surpluses for their further expansion programs. They were supposed to work for social welfare and industrialization. Profit-making was not their main motive. But due to the liberalization and privatization policy, the situation has changed. Now, they have to justify their existence through positive results. They have to earn surpluses like private concerns for their survival. Later on, the CPSEs performed poorly, started incurring losses, and became deep swamps of inefficiency. They had become a fiscal burden for the country. They were taken to be the ‘white-elephants’. This paved the way for disinvestment/privatization.

Is Disinvestment Like Killing The Golden Goose?

CPSEs have been engaged in the manufacture of goods and provisions of services in almost all the important spheres of economic activity.

Union finance minister Nirmala Sitharaman.

Advertisement

Financial Performance

Let us delve into the performance of CPSEs during the last two years. Their performance is a mixed bag. According to the Public Enterprise Survey 2020 tabled in Parliament in August 2021, at present, there are 366 CPSEs. Among 256 operational CPSEs, 96 are under construction and the rest 14 are under closure and/or liquidation.

Out of operational CPSEs, one-third i.e. 84 CPSEs reported an aggregate net loss of Rs 0.45 lakh crore in FY20. The surprising thing is that the total loss in FY 20 has jumped by 41.7 per cent. against the total loss of FY19. Two third – 171 enterprises in the core sector of the economy had made a profit and are functioning efficiently. They reported an aggregate net profit of Rs 1.38 lakh crore for FY20. One CPSE was at the break-even level.

The overall net profit of operating CPSEs during the financial year 2019-20 slid by 35 per cent and reached Rs 0.93 lakh crore against Rs 1.43 lakh crore in FY19. The major reason for the fall in profit was attributable to the petroleum cognate group where it reduced to Rs 0.03 lakh crore in FY20 from Rs 0.32 lakh crore in FY19. Other cognate groups which exhibited a decline in profit were crude oil, heavy and medium engineering, telecommunication, IT, financial services and agro-based industries.

Advertisement

The CPSEs generated a profit of 4.32 per cent against the investment of Rs 21.59 lakh crore during FY20. In FY19, they had generated 8.0 per cent profit against an investment of Rs 17.83 lakh crore.

A debate is on how long the public could be taxed for the inefficient operations of these CPSEs? The 9th Finance Commission had also shown their deep concern about low returns against the huge investments made in CPSEs. It should be an engine of growth rather than a drag on government resources. It was suggested by the commission that possibilities should be explored for restructuring and phasing out loss-making units in the non-core sector by an appropriate package of measures.

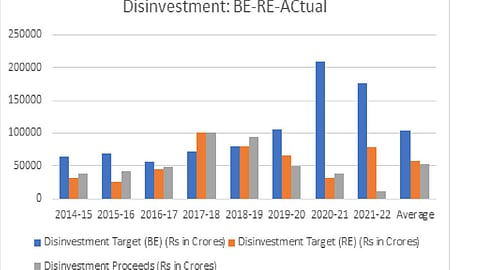

Disinvestment - BE-RE-Actual Proceeds

India had opted for the policy of disinvestment through the industrial policy of 1991. The budget target of disinvestment has been achieved only six times. It seems that while fixing the target, it is not taken considered whether it will be achievable or not. The government has set the target for realizing Rs 1.75 lakh crore in FY22 was further slashed by about 55 per cent and fixed the revised target of Rs 0.78 lakh crore. However, the actual realization is only Rs 0.12 lakh crore so far for the current financial year.

Advertisement

Even this sum is realized because of the realization of Rs 2700 crore from the privatization of Air India. It indicates both budget and revised estimates are out of reach while the disinvestment of BPCL and others may not complete by this fiscal. The disinvestment proceeds are only 6.9 per cent of the Budget estimate and 15.4 per cent of the revised estimate. For FY23, the government has set the target of disinvestment of Rs 0.65 lakh crore.

If we talk about the performance during the last eight years, it is the sixth time when the government did not achieve the budget target. Apart from that, the government has revised the target seven times since FY15. The silver lining is that the revised target has been achieved every time except in the FY20 and current fiscal. In the last budget, FM Nirmala Sitharaman came out with a big-ticket Strategic Disinvestment Policy 2022.

Advertisement

The government had announced the privatization of a number of Central Public Sector Undertakings. Disinvestment of BPCL, Air India, Shipping Corporation of India, Container Corporation of India, BEML, IDBI Bank, Pawan Hans, Neelachal Ispat Nigam Limited (NINL); the privatization of two public sector banks and one general insurance company would be completed in 2021-22. However, this seems improbable now, as only 25 days are left in this financial year.

However, the emergence of the Covid-19 pandemic halted the pace of the government’s ambitious privatization plan. Except for Air India, no privatization transaction took place in the current fiscal. The government did not introduce the public sector bank amendment bill to initiate the privatization process of two PSBs. The only point of satisfaction is that the strategic partner of Neelachal Ispat Nigam Limited has been selected and DRHP of LIC has submitted to the SEBI. However, LIC-IPO is likely to be delayed until the next financial year due to the Russia- Ukraine crisis.

Advertisement

Disinvestment Vis-à-Vis Fiscal Deficit

Disinvestment proceeds have been persisting to an important component in fiscal mathematics. The size of the fiscal deficit depends upon the realization of disinvestment proceeds. Missing the target not only reduces capital receipts, but it also affects the number of fiscal deficits.

The government had set the fiscal deficit target of Rs 15.07 lakh crore – 6.8 per cent of the GDP for the financial year 2021-22. Due to the under realization of the disinvestment proceeds against the target, the size of the fiscal deficit of the current fiscal could have been much larger.

However, as per the financial budget for FY23, the number is under control. It has reached Rs 15.91 lakh crore – 6.9 per cent of the GDP. The buoyancy in tax revenue and dividend and profits from CPSUs and RBI and public sector banks offset the shortfall of proceeds from disinvestment against the target.

Contribution To Central Exchequer

Despite the poor performance of CPSEs in terms of profit in recent times, the majority of CPSEs in the core sector such as ONGC, Coal India Ltd, Power Grid Corporation, NTPC, GAIL, Mahanandi Coalfields, Power finance corporation, etc are functionally efficient and are making a substantial contribution to the exchequer by way of excise duty, customs duty, GST, corporate tax, Interest on Central government loan, dividends and surplus, and other duties and taxes. Their contribution to the exchequer was Rs 3.76 lakh crore in FY20. Their contribution in terms of dividends and surplus during FY18 to FY22 may be seen in the table below.

During the last five years, the government has received an average of Rs 1.27 lakh crore per year from dividend and surplus and through disinvestment, realized at an average of Rs 0.59 lakh crore per year. The government has set the target of generating Rs 0.65 lakh crore from disinvestment of CPSEs, on the other hand, the government expects to generate Rs 1.14 lakh crore from dividend and surplus from CPSEs, RBI, nationalized banks, and financial institutions (excluding revenue from taxes and interest) in FY23.

Thus, if substantial share-holding of the government in profit-making CPSEs is disinvested, it will lose dividend/surplus income. Privatization of profit-making units, according to former Dy CAG – Dr. B P Mathur, would be like a case of killing the goose which lays the golden egg. Therefore, loss-making units should be the first candidates for privatization and if there are no buyers they should be closed/liquidated after taking care of workers’ interests.

(Vinay K Srivastava teaches at I.T.S Ghaziabad. He is the co-author of Indirect Tax Reform in India and Co-editor of the Future of Indian Economy – Past Reforms and Challenges Ahead.)