Partner and Leader, Personal Tax, PwC India

Budget Focuses On Farmers And Poor

Budget has announcements for agriculture & rural sectors, but expectations of salaried class have not been met

Budget Focuses On Farmers And Poor

Advertisement

Amidst high expectations from various sections of society, the Finance Minister presented his last full-fledged Budget before the next Lok Sabha elections. Be it the common man or the high net worth individuals, senior citizens or the women, everyone was hoping for something. But the government paid attention to the farmers and the poor. There are several proposals for the farmers and the poor in this budget, which are expected to look after this section of the society well. Although the salaried class seems to be left with raised eyebrows, as nothing went into their pocket, the government believes they indeed did something for the salaried class in the past during its current term and farmers and the poor are the priority at this moment. Senior citizen category of tax payers is likely to cheer as there are several proposals benefitting them, which they have been expecting for a long time. In this article, we try to explain the impact of key proposals on individual tax payers.

Advertisement

Salaried class

No change in personal tax rates: There is no change in tax slabs and tax rates. There were expectations to increase the basic exemption limit, particularly after the Economic Survey indicated an addition of 1.89 million new tax filers post demonetisation and an addition of 3.4 million new tax payers since the introduction of Goods and Services Tax (GST).

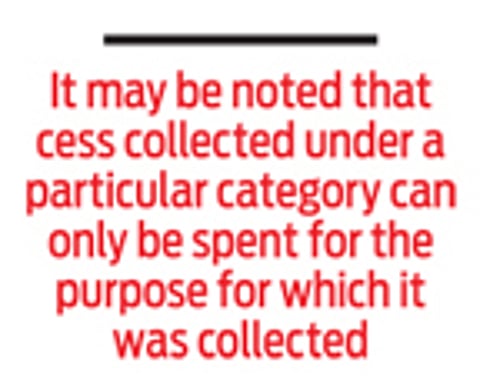

The FM has proposed to replace the existing three per cent education cess by a new four per cent ‘Health and Education Cess’. The move will help to collect a little more and at the same time, categorising it under Health and Education Cess will help to provide funds for the welfare measures as announced in this Budget for health and education. It may be noted that cess collected under a particular category can only be spent for the purpose for which it was collected.

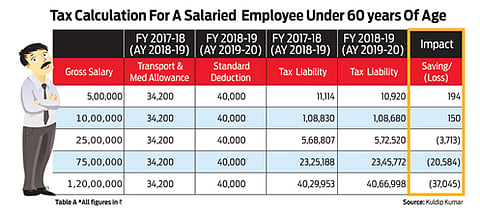

Reintroduction of standard deduction: Reintroduction of standard deduction of `40,000 was expected to bring smiles on the faces of salaried taxpayers, but they soon realised that the tax benefit will be greatly nullified due to withdrawal of tax benefit in relation to transport allowance of `1,600 per month and medical reimbursement of `15,000 per annum. Perhaps the move to introduce standard deduction is to extend the benefit to the 2.5 crore pensioners (senior citizen category)—the government wanted to put more money in their pockets. Nevertheless, this proposal will free the taxpayers and the employers from the administrative burden of collecting and retaining the bills for medical reimbursements. Table A shows how the above proposal impacts the various taxpayers falling under the different income groups.

Advertisement

One may note that those falling in the lower income groups will have negligible impact. But those in higher income groups will be required to shell out more.

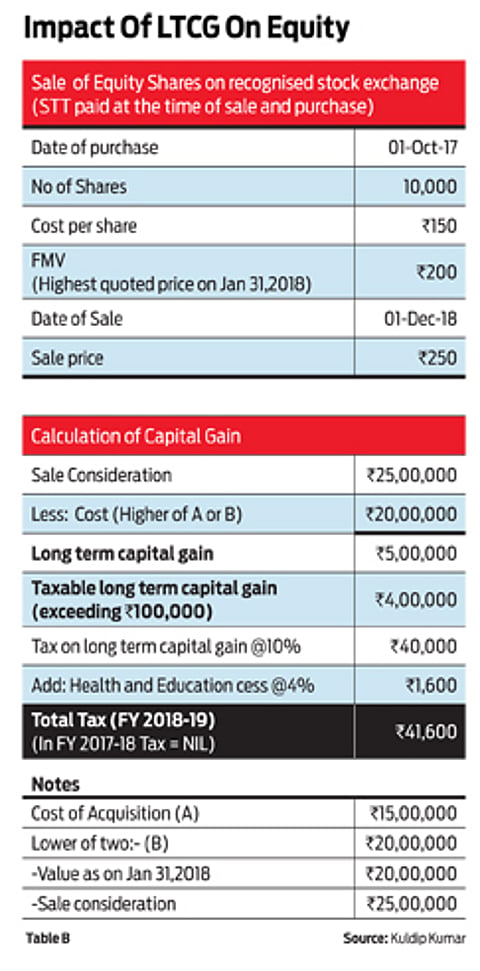

LTCG from sale of equity shares: This is the only asset class that has been doing well this year and how could it have escaped the attention of the government from collecting some piece of tax out of it? In fact, this fear was not unfounded by the tax payers as the Prime Minister had hinted at this tax long time back in one of his speeches. Yet, people were not expecting this to happen as the government has already formed a task force to review re-writing of the decades-old Income Tax Act, 1961. Such structural changes were perhaps expected later when re-writing would happen.

The FM has proposed to tax the long-term capital gains (LTCG) on sale of equity shares and equity-oriented mutual funds listed on recognised stock exchanges in India and subject to STT (Securities Transaction Tax) on both sale and purchase. Such gains exceeding `1 lakh are proposed to be taxed at 10 per cent (without indexation), which are presently exempt from tax. However, the appreciation accrued until January 2018 has been protected due to grandfathering provisions. Small investors with LTCG not exceeding `1 lakh would also remain unaffected. Calculation of taxation of LTCG is illustrated in Table B.

Advertisement

Dividend Distribution tax on equity oriented mutual funds: If you are an investor in any equity oriented mutual funds, your future returns from such funds may be tempered as the FM has proposed to charge dividend distribution tax (DDT) at 10 per cent on equity oriented mutual funds. Presently, no DDT is levied on these schemes.

Senior citizens

If anyone has to be happy with this Budget, it is the senior citizen tax payers. There were long standing demands to protect their earnings in the declining interest regime, as senior citizens park their funds largely in fixed return saving schemes. They are also required to spend money on routine medical check-ups and they needed a tax deduction for such medical expenditure. To some extent these expectations have been met in this Budget.

Investment in Pradhan Mantri Vaya Vandana Yojana: Investment cap in Pradhan Mantri Vaya Vandana Yojana (PMVVY) has been raised from `7.5 lakh to `15 lakh. This scheme offers assured 8 per cent return on the investments. Hence, this move will provide an opportunity to the senior citizens to earn assured higher interest by investing more.

Advertisement

Health insurance and medical expenditure (Section 80D): The monetary limit for deduction covering payments towards premium on health insurance policy or preventive health check-up or medical expenditure with respect to senior citizens is proposed to be increased from `30,000 to `50,000. Further, expenditure on medical treatment will only be covered where the concerned senior citizen is not covered under a medical insurance (insurance cover condition). Presently, only those who are aged 80 and above are eligible to avail deduction for medical expenditure, if they are not covered under medical insurance. This is a good move and will help those senior citizens who do not have medical insurance cover. Others would need to evaluate whether to take the medical insurance cover to buy protection for major medical expenditure or avail the deduction for the medical expenditure.

It would have been good to do away with the insurance cover condition as, presently, medical insurance is really needed for protection against future medical expenditure. What they needed was an additional deduction for the day-to-day medical expenditures, such as medical tests, physiotherapy and so on.

Deduction for medical treatment: At present, deduction is available to senior citizens for the medical treatment of specified diseases (neurological diseases, hematological disorders etc) to the extent of `60,000 (`80,000 for very senior citizens), subject to certain conditions. The Finance Minister has proposed to enhance the limit to `1 lakh for both senior as well as very senior citizens tax payers.

Deduction for interest from deposits: This year, the Budget has introduced a deduction of `50,000 on interest earned by senior citizens from fixed deposits, recurring deposit and saving bank accounts. Presently, deduction is available upto `10,000 to all tax payers including senior citizens in respect to the interest they earn from saving bank accounts.

The new proposals in the Budget are likely to result in more savings in taxes for the senior citizens falling under different income group (Table C).

Simplification and procedural changes: E-assessment was tested initially in metro cities on a pilot basis and, thereafter, it was extended to 102 cities. This year, the Budget has proposed the implementation of e-assessment across the country. It has been proposed to notify a new scheme for this project. This will greatly facilitate the ease of interaction with the tax authorities where sometimes tax payers fear to visit the tax office physically. Further, tax authorities will no longer be able to make any adjustment in returned income on the basis of income appearing in tax credit statement (form 26AS) or tax withholding certificates (form 16/16A) at the time of summary assessment. This will apply for the financial year 2017-18 onwards and will avoid filing of unnecessary rectification applications by the tax payers.

Tax-free withdrawal from National Pension Scheme: The Budget has proposed to extend the exemption of 40 per cent of the total amount payable to non-employees subscriber on closure of NPS account or opting out of the same. Earlier, this exemption was available to employee subscribers only. This is a welcome move. However, the Budget has not extended the similar exemption to the non-employee subscribers on their partial withdrawal, which is presently available to employee subscribers only. This is something which may require a relook.

Restricting exemption under Section 54EC to sale of land or building or both: The provisions of Section 54EC provides exemption from LTCG on sale of any asset, if the specified bonds are purchased within six months from the date of sale of asset. There is also a cap of `50 lakh per annum. It is proposed to restrict the said exemption only to LTCG from land or building or both. Further, the holding period for the specified bonds is also proposed to be raised from three years to five.

Taxation of capital gains from immovable property: Presently, while taxing the capital gains (Section 50C), business profits (Section 43CA) and other sources (Section 56) arising out of transactions in immovable property, higher of the sale consideration or stamp duty value is adopted. This results in taxation of difference as income in the hands of both, namely buyer and the seller. The finance minister has proposed that no adjustments shall be made in case the variation between stamp duty value and the sale consideration is not exceeding five per cent. This will really provide an ease in case of genuine transactions and unnecessary litigation for a small difference.

To sum up, while senior citizens have been looked after well, the salaried class may perhaps not be happy with this Budget. It looks like the expansion of tax base for income tax and the GST might not have given enough confidence to pass on some tax relief to the salaried class. Although the finance minister indeed recognised that 1.89 crore salaried tax payers paid taxes of `76,306 on an average, the individual businessmen, who almost equal the salaried individuals in numbers, paid taxes of `25,753 on an average. The tax authorities will continue to focus more on compliance to improve tax collections.

One strong message the government has given through this Budget is that they are sensitive to the farmers and the poor section of society, which is perhaps needed as well. Future will tell how this government will walk the talk. Every big journey begins with a small step. If the government succeeds in implementing the proposals as envisaged for the farmers and the poor, it would be a great step in building a new and better India!

The author is Partner and Leader, Personal tax, PwC India

(The views expressed are personal)