Natco Pharma is a midsized pharmaceutical company with a presence across the pharma value chain. Incorporated in 1981 and headquartered in Hyderabad, the company has been an expert in formulating innovative dosage forms. It has five formulation locations across India and two chemicals manufacturing locations. The company’s R&D facility is its strength which is certified by global regulatory authorities. Natco has its presence across segments including domestic and international formulations, API manufacturing and drug discovery.

A leading player in the domestic oncology segment, it has attained this position by making decisive therapies affordable. The oncology products have become the preferred recommendation by oncologists for patients. Natco’s products reach to more than 40 countries, which has been possible through its partnership driven model.

Its oncology portfolio is catering to breast, brain, bone, lung and ovarian cancers. As on December 2016, the company has 43 niche Abbreviated New Drug Application (ANDA) filings in the US and is targeting to file 10 plus ANDAs in the US during the next two financial years.

2 March 2026

Get the latest issue of Outlook Business

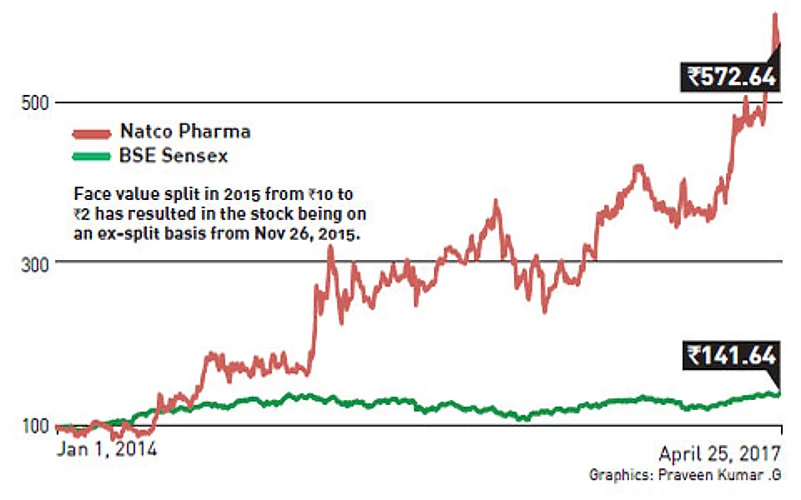

Financial scorecard

In terms of revenue segmentation, company’s domestic formulations contributed 52 per cent, followed by international formulations at 14 per cent, API’s segment contributed 14 per cent and the remaining was by others. The company in terms of its net revenue clocked a compound annual growth rate (CAGR) of 21.3 per cent over FY 2012-16. Company has demonstrated growth with its widening product portfolio over FY 2012-16, which led to revenue and profit after tax (PAT) clocking a CAGR of 21.3 per cent and 27.4 per cent.

The company has recorded consolidated total revenue of Rs 685.13 crore for the quarter that ended on December 31, 2016, as against Rs 293.45 crore during the same quarter previous year, registering an increase of about 134 per cent. The net profit saw a whopping growth of 425 per cent in Q3 FY 2017 against Q3 FY 2016. The revenue and profit growth for the company during the quarter was driven predominantly by sales of Oseltamivir in the US market.

The company has also launched new cardiology and diabetology division for the Indian market, where it expects to attract significant market share, given the demand in both these segments, making it an attractive pick.

Why Buy?

- Consistent growth across all key indicators

- Niche acquisitions in the US and other countries

- Leading player in the oncology segment

Watch Out

- Delays in ANDA approval is risky

- Currency risk needs to be factored given global operations