Kotak Mahindra Bank (KMB) acquired ING Vysya Bank in November 2014, thus expanding its footprints in south India. Since the bank already had a significant presence in the western and northern markets, this deal made KMB the fourth largest player in the private banking space.

Financials

3 February 2026

Get the latest issue of Outlook Business

KMB in its third quarter earnings of FY16 posted a jump of 32 per cent in consolidated net profit at Rs.945 crore as against Rs.717 crore, in the same quarter a year ago. The numbers are not comparable with the previous year’s performance as the bank merged ING Vysya Bank with itself with effect from 1 April, 2015. However, the strong demand for loans from companies and industries boosted the bank’s profits even as it continued to make provisions towards the loan book of erstwhile ING Vysya Bank.

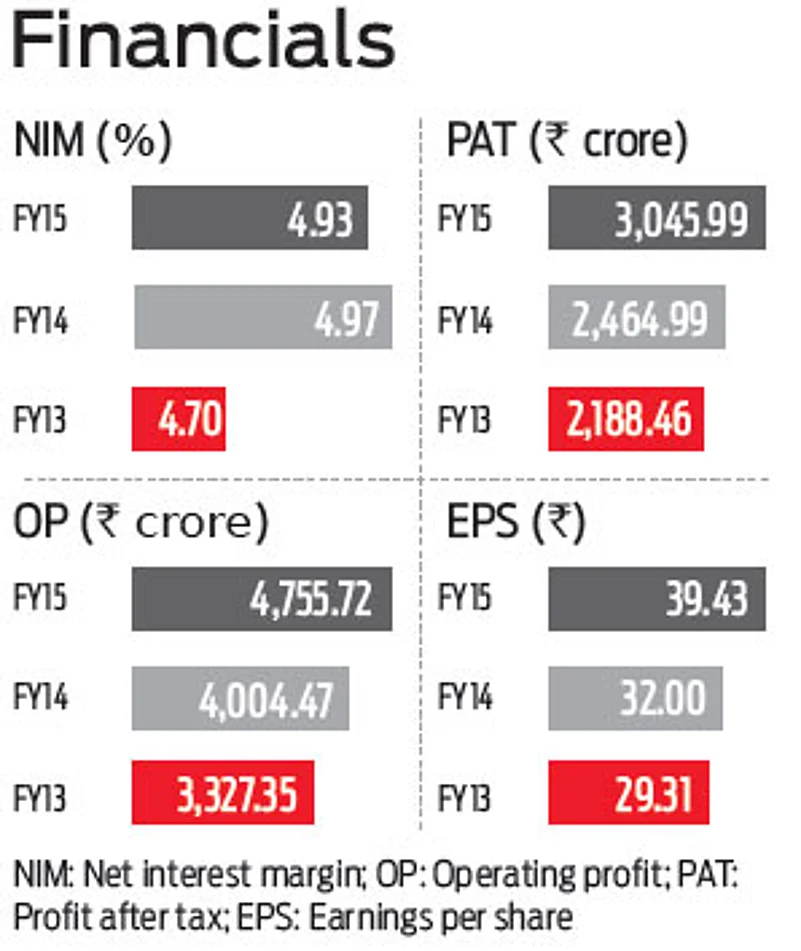

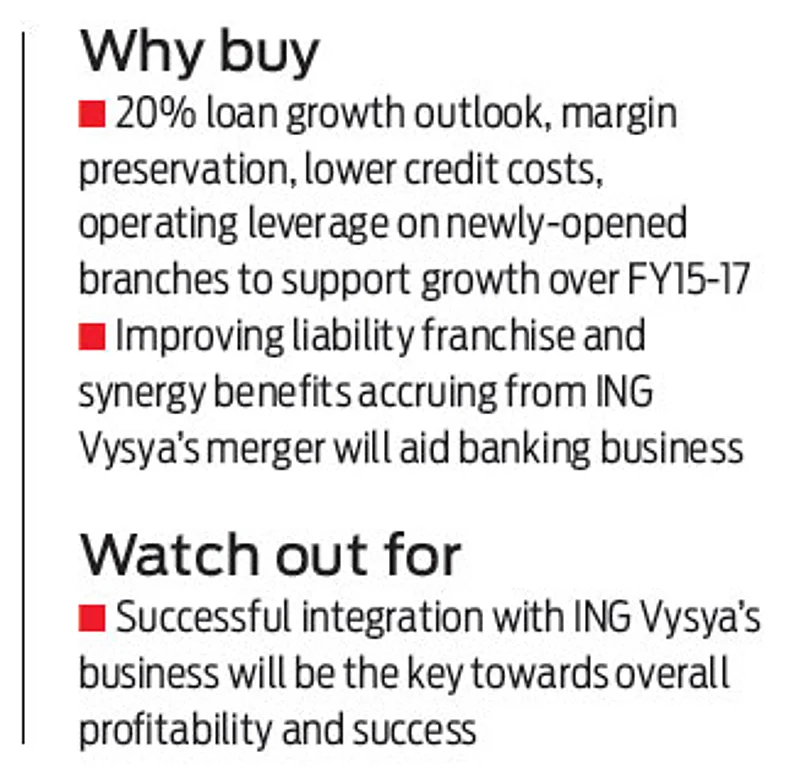

The bank’s current loan book post merger stands at Rs.1,41,136 crore while it was Rs.86,058 crore in third quarter of FY15. Out of this, bad loans on a net basis (net NPA) stood at 85 basis points, up two basis points over the third quarter of the last fiscal. The management expects to see a robust 20 per cent loan growth for FY16. It also reported a net interest margin (NIM)—the difference between the interest it got on loans and that it paid on deposits— of 4.4 per cent on a consolidated basis. KMB today enjoys having the highest NIM in the private sector banking space, beating peers such as HDFC Bank, ICICI Bank and Axis bank in this regard.

Way forward

The intense competition among private banks has led to their digital transformation. KMB’s digital payments transactions crossed 15 lakh in

December 2015. The synergy from the merger is also expected to reflect in return ratios from mid FY17.

In July 2015, it rewarded its shareholders with a 1:1 bonus issue and has been quoting ex-bonus from July 8, 2015. It has posted 2 per cent returns from January 1, 2013, till January 21, 2016. Going forward, the strong core capitalisation, along with superior margins and asset quality, coupled with improving franchise and synergy benefits accruing from ING Vysya’s complete merger from Q1FY17, will strengthen its position. Investors with a medium- to long term horizon can invest in KMB.