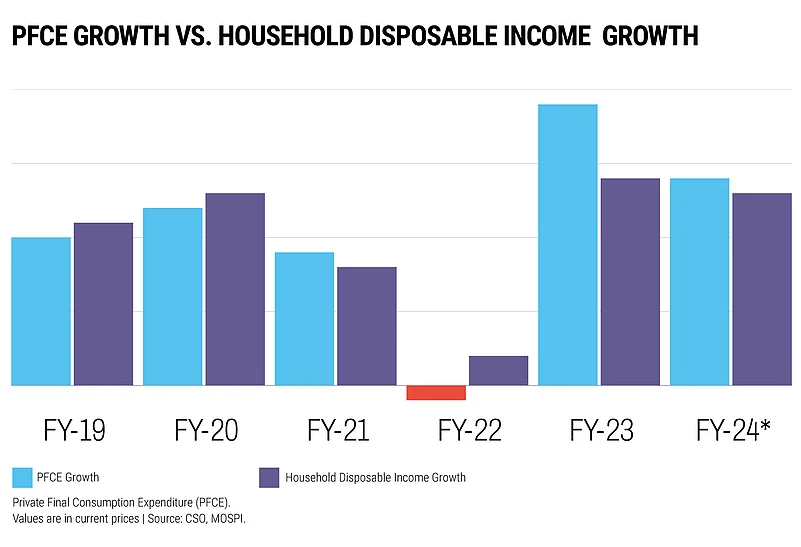

The first signs of financial strain began with the pandemic in 2020 as households’ expenditure on consumption started to outpace their growth in disposable income

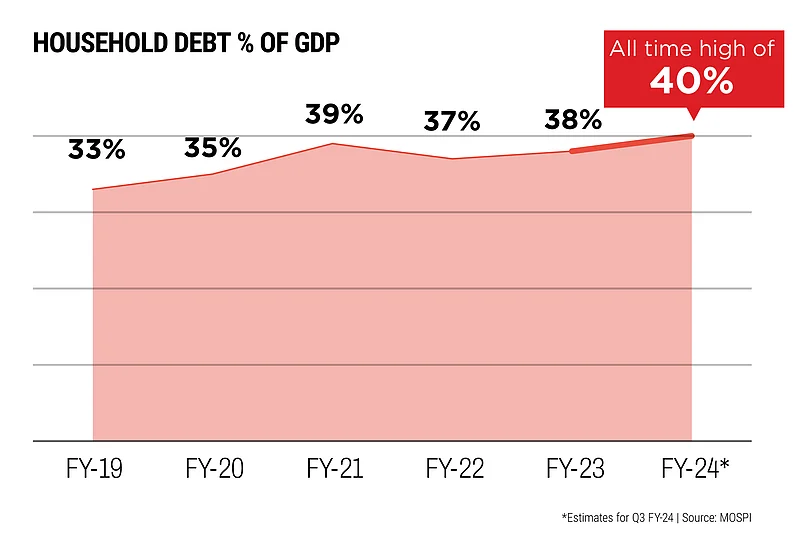

Household debt hit a record high in FY24, reflecting a change in consumer behaviour to take on a higher leverage

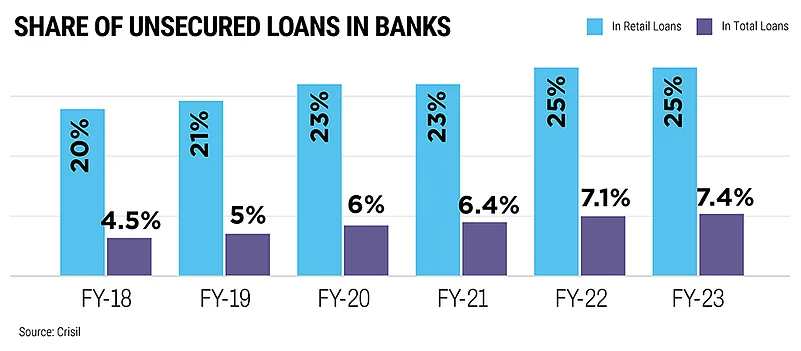

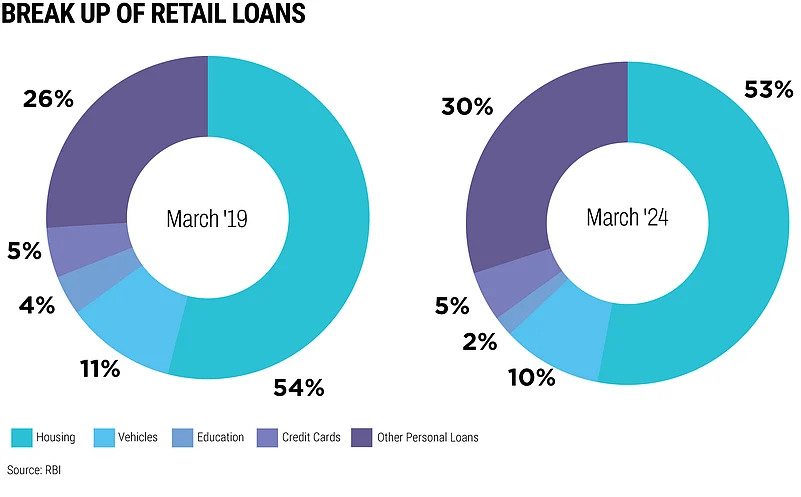

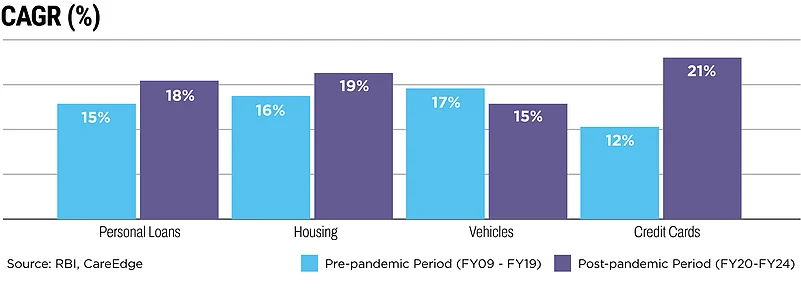

A closer look shows that unsecured retail loans, including credit card usage, went up in the post-pandemic period. Driving this surge was the rise in fintech companies that provide personal loans to younger borrowers through simplified processes and faster approvals

3 February 2026

Get the latest issue of Outlook Business

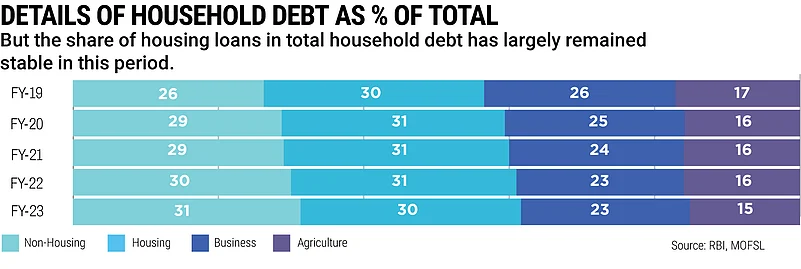

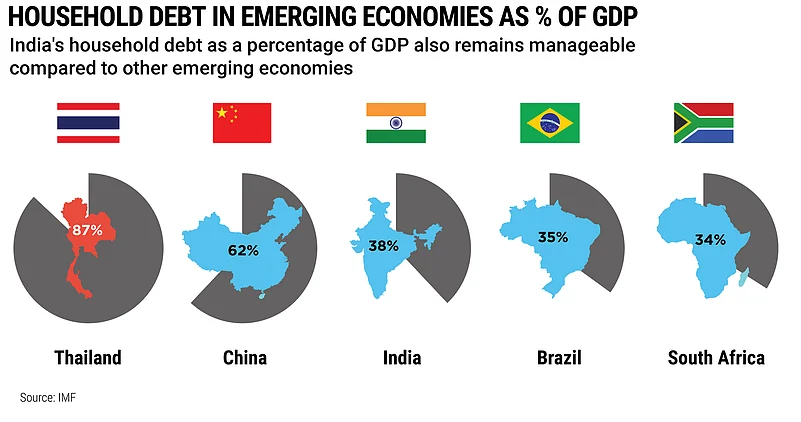

The growing reliance on borrowing may not be an immediate concern as home loans continue to be the dominant driver of household debt, but monitoring unsecured lending from fintech and non-banking financial companies is crucial

Home loans are secured and more productive as debt is invested in appreciating assets. The demand for home loans has also remained stable and non-speculative, lowering the risk of a housing bubble

Research: Kush Sharma, Graphics: Shriya Bhatia