In an interview with Outlook Money, Ajay Srinivasan, CEO, ABFSG, tells how his company is trying to be the best in every product category. Excerpts:

Can you take us through what Aditya Birla Financial Services Group (ABFSG) has done in the last few years and where does the customer sit?

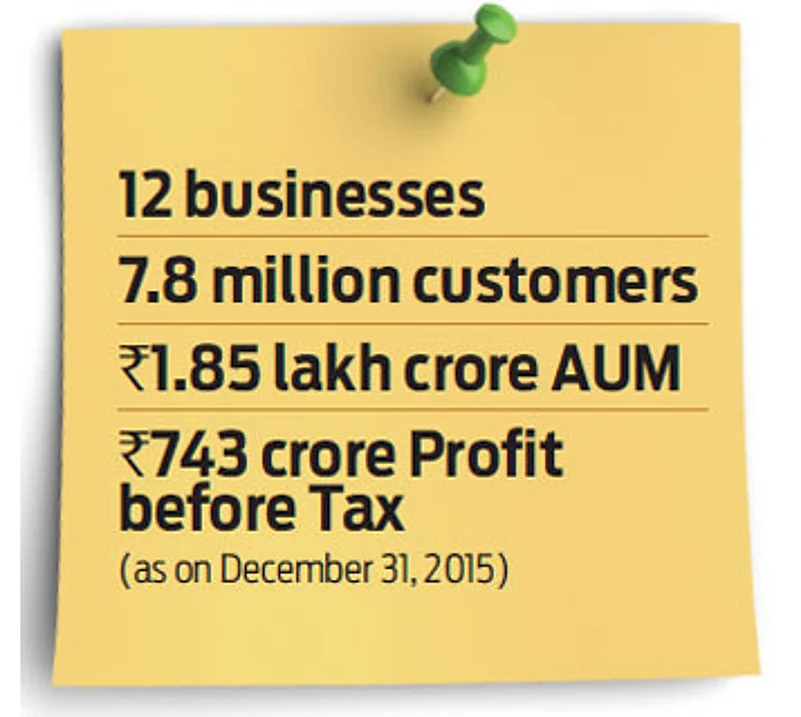

ABFSG is an umbrella brand that encompasses a number of financial services. We have individual legal entities that provide different products and services as required by regulation and law. But ultimately we want to be able to provide end-to-end services to our customers through their lifecycle. So, under Aditya Birla Financial Services, we have life insurance, asset management, we provide private equity, lending products and we will soon have health insurance.

3 February 2026

Get the latest issue of Outlook Business

We look at the customer needs broadly in three buckets: those who have money and don’t know what to do with that money, those who need money to achieve their financial goals and those who see some risk or the other to protection against that risk. And all our products fall under these three buckets. Some of these we manufacture, some of these we manufacture and distribute, and some of these we purely distribute.

In terms of scale and size, financial services have grown over the last 7-8 years. We multiplied our revenue by 4 times and our assets have gone up 8-8.5 times.

The trend earlier was for banks to get into a plethora of financial services. In contrast, ABFSG is a mix of several entities, with banking missing the list.

What we are looking to do is to have businesses which have the potential to be leaders in each sector. If you look at any of the industries we are operating, you know the top 5 and 10 players account for bulk of the economics in the business. So, leadership is the focus.

In financial services there is nothing tangible, you sell trust. Consumers, therefore, look for the people they can trust. That made us think about how we build each of these product and services so that we can give customers what they need. I don’t think one-stop means you will get everything from one end; you have to be best in each of your products. So if I have a mutual fund product that doesn’t mean anybody can buy life insurance from us. We have to be best in each and every product and services.

Two pieces which I feel are missing at this point of time are general insurance and health insurance. Will these come up later?

We are entering health insurance. It will be a joint venture with a South African company—the MMI Group, with whom we have signed an agreement. We will be able to launch this business somewhere during the course of this year. Health insurance is really a big opportunity in India because if you look today, 60-70 per cent of heath expenditure is typically out of pocket by the individual. Social security doesn’t really exist in this country.

If you leave health insurance, the largest opportunity is in motor insurance that we offer our customer through our general insurance broking business. Our customer gets access to the product but we are not manufacturing, we are only distributing it. We look at all these products and services and figure out which one we should manufacture competitively and if we think we can’t manufacture it competitively, we will provide them as a distributor to our customers.

Financial services, especially financial advisory, are being regulated by advisory models such as SEBI- RIA. Do you see yourself in that space as well as investment advisors or just as a distributor.

At this moment we would like to remain as distributor but I think customers need advice considerably. I think therefore if we are distributors then customers would want advice from us. In this business those who provide better advice to their customer will go forward.

What is happening on the NBFC front?

We are among the few who are diversifying their NBFC. Our view is that there is opportunity to grow in a number of areas. There is risk benefit in diversifying, like we see opportunity in SME financing. We think that is the area where we will continue to grow as opportunities for entrepreneurs grow; and finance in SME will also grow. Housing finance is the second area we will focus in the lending area.

How much is information technology driving your business now?

We are putting a lot of effort on it and it gives us reach that we might otherwise may have not got, so the whole technology of reaching somebody on a phone today gives us reach that we otherwise would have not been able to get as a provider ourselves. That’s straightaway revenue opportunity for us; it improves efficiency and effectiveness because you know people are using technology, which allows them to have more free time to do other stuff.

We are enabling sales people with tech tools which let them spend less time doing operational work and give them more time to sell. And I think it will allow us to get cost benefit too.

Where does MyUniverse fit?

Aditya Birla MyUniverse, to my mind, is a very innovative idea. The logic behind MyUniverse, which is really a personal financial management portal, was that we saw two things that we were missing as an opportunity. We saw this huge growth in internet and we saw also that it is going to provide an opportunity to people to do things differently to what they have done before.

This allows us to attract younger customers and leverage the growth of internet. Today, through MyUniverse, you can aggregate your financial information in one place, you can get advice on what you should do with your financial information, and also transact. I think that end-to-end solution is still very unique in this market.

As a prospective customer, why should I come to ABFSG when there are so many others?

I think there are three things you should come to us for: we are someone who has been trusted and who has a brand that has been recognised and we believe in fairness and equity in terms of dealing with customers. When it comes to financial services, it is a very important ingredient. So trust and faith is the first reason why you should look at ABFSG. The second is the product range and performance of the product.

We have pride in performance of our products whether it is mutual funds, lending products or insurance products. They all are performing to their best of class. The third is the whole issue of service. Expecting that when you come to us you get service that makes you feel that it is worth doing business with us.

We are shifting from a ‘buyer beware’ model to a ‘seller beware’ model. Considering the various businesses you operate in, how do you safeguard yourself?

I think you have to do it at two levels. You have to make sure that the communication received by customer from you is adequate so that the customer understands what he is buying and you have to work through the distribution channel to make sure that they are providing right information to the customer.

At the backend we do our own checks in terms of suitability and appropriateness of the product so that products are not put in the wrong bucket. But I think what is understated in this whole discussion and debate is the role of the individuals themselves. In my view the individual has to take much greater responsibility for the financial planning that they do for themselves for the financial products that they buy. I don’t think that you can expect that diligence to be passed off to someone else always.

You have got a payment bank licence. Tell us about it.

Our payment bank licence is a joint venture with the telecom company, Idea. So our view is that it is like a pipe available to us. It’s a pipe reaching to the smallest part of India and to a number of customers. How can we define products and services that can flow through these pipes and reach the customer is what we will be looking to devise the products and services around.

nk@outlookindia.com