“If winter comes, can spring be far behind”- PB Shelley’s famous quote reminds me of the capex conundrum we are facing today. With a lot of focus on missing capital expenditure by Indian corporates in the past, there have been signs recently that spending on capex has increased in some sectors.

Optimism in the economy is visible in many ways, especially the ongoing buoyant performance in both equity and debt markets. The low duration and credit spread in the corporate bond market demonstrate the confidence of stakeholders in the underlying economy. At the same time, the strongest banking sector balance sheet in the decade mirrors the improvement in borrowers’ credit profile.

Indian corporates have been shying away from large capex for close to a decade, affected by the stretched balance sheet of borrowers as well as lenders and a deluge of economic shocks, especially pandemic and geopolitical conflicts. The improvement in balance sheets has led to an uptick in capex recently. However, the signs of a broad-based capex cycle are still missing amid multiple uncertainties.

3 February 2026

Get the latest issue of Outlook Business

Improving Indicators

The corporate credit profile in the past two years has exhibited one of its strongest performances in over a decade. The strong earnings momentum is also to be seen in the backdrop of a period which witnessed significant deterioration in the global economic conditions. Consumption-led domestic demand (premium segment) and investments (mainly government capex) contributed to the business growth. Transmission of commodity prices to end-customers helped corporates sustain profits amid stubborn inflation and rising interest costs. Indian companies’ performance in the global markets also improved due to strong demand from US and supply chain diversification away from China. These factors led to highest-ever exports. Amid the doom and gloom of the global economy, Indian markets continued to post strong growth as corporate India emerged as a shining spot.

Implementation of production linked incentives (PLI) scheme of the government has helped segments like electronics, network & telecom equipment, white goods, pharmaceutical and automobiles. On the other hand, the response to sectors such as textiles, specialty steel, ACC batteries and solar PV modules has not been encouraging. The shift of policy framework from “low value-add assembling activities” to “high value-add futuristic manufacturing activities” has been a step in the right direction which would help in making Indian manufacturing future ready, although benefits of such measures would be back-ended and may not be visible in near term.

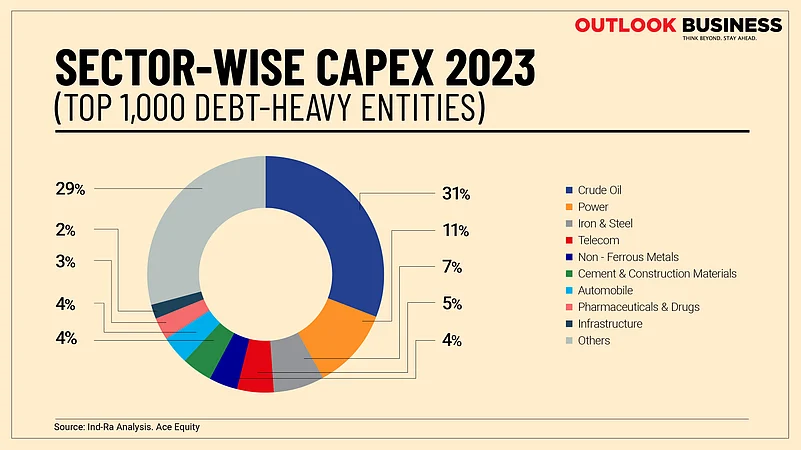

Preliminary data of the top 1,000 debt-heavy corporates (contributing over three-fourth of private corporate capex) suggests that spending on capex gained traction in FY23, amid multiple uncertainties. The data indicates that large capex activities have been concentrated in sectors such as oil & gas, iron & steel, and telecom, whereas sectors such as cement, chemical, auto ancillary and textiles have shown capex spending in pockets.

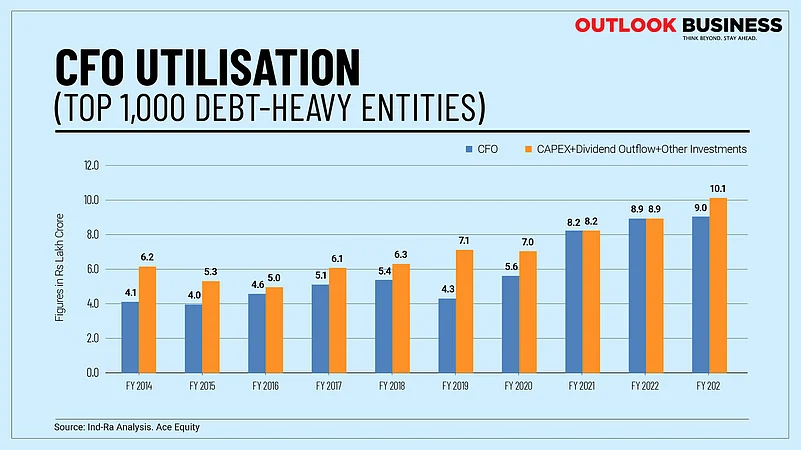

The gap between cash flow from operation (adjusted for interest payment) and committed spending (capex + dividend + other investments) has come down recently, with a likely modest pickup in FY24. This suggests that corporates are incurring capex without raising debt. Moreover, the data shows that corporates will need to take some leverage or spend on capex to ensure healthy ROE (return on equity) on a sustained basis.

While the industry is incurring focused capex as of now, there are certain challenges it is facing which is preventing a broad-based capex cycle.

Hurdles To Capex

Looking at the current situation, it appears that large capex would continue to be restricted to the entities having strong parentage and a strong credit profile. For a broad capex cycle, demand certainty or visibility of strong future demand is a necessary condition. The current situation is not conducive due to rising interest rates domestically and globally, uncertain export demand, elevated geopolitical situation, and lagging broad-based domestic consumption demand. Moreover, the capacity utilisation level is still hovering around 75 per cent, although some entities are operating at close to 100 per cent. In addition to this, the duration of interest rate and commodity cycles has shortened over the past decade. These are some of the major deterrents for many medium-sized corporates, who had passed through the worst corporate cycle in recent time between FY13 and FY19.

Even for large corporate entities, one of the key factors that can affect their capex in the coming financial years would be their spending on green transition. The largest effect would be felt by production-oriented industries, such as metal, power, auto ancillary, and specialty chemicals. Without meeting the global norms, there could be an impact on access to global finance and on exports. At some stage, domestic lenders would also be following the same practice, therefore stricter adherence to ESG norms would be required in the coming years. From FY24 onwards, few granular disclosure norms from domestic regulators and export bodies will also start coming into force, prompting corporates to start chalking out a trajectory for eventual green transition.

For now, it appears that a reasonably good capex cycle by large entities in sectors like energy, logistics, iron & steel, telecommunication might be around the corner as corporates leverage their improved positions. However, more needs to be done to help medium size corporates which would help in bringing a broad-based capex cycle soon.

With the support of Sagar Deasai, senior analyst at India Ratings & Research.

(Soumyajit Niyogi is a Director at India Ratings & Research. The views expressed here are his own and do not reflect those of the organisation)