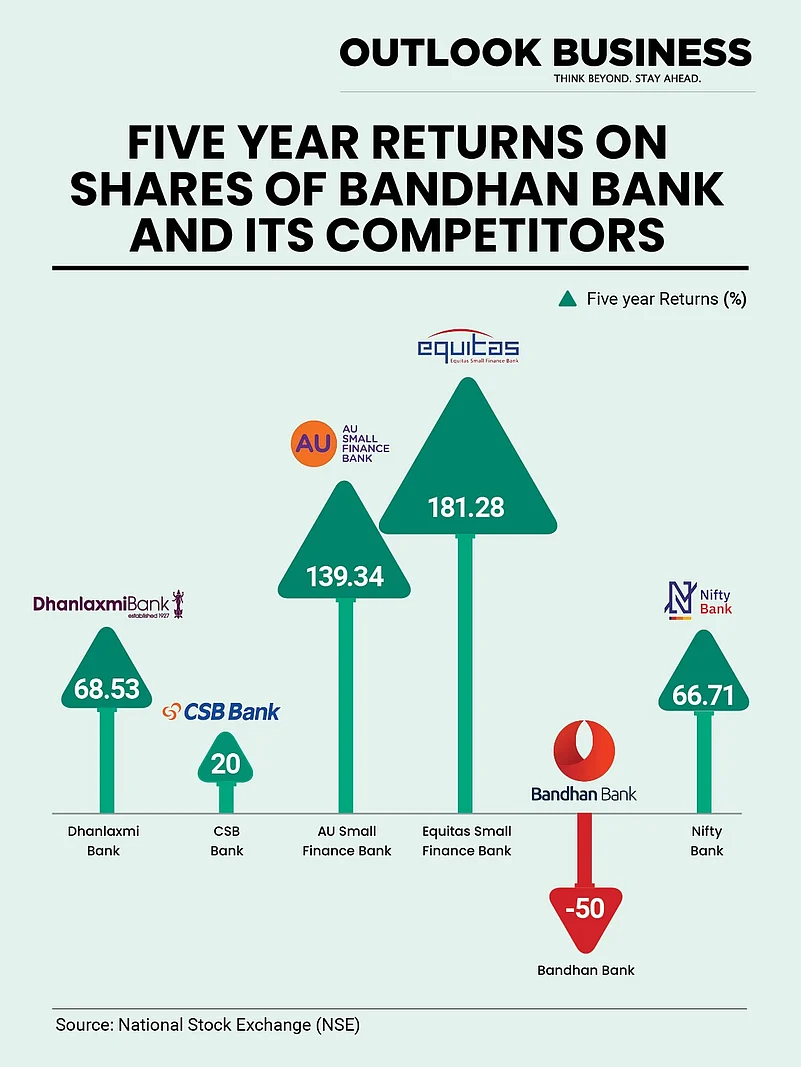

Bandhan Bank’s story on the bourses so far has been one of disappointment. After a promising start in 2018, its stock has fallen over 70 per cent from its all-time high of Rs 741 touched in August 2018. The Kolkata-based bank was listed at a 27 per cent premium on the bourses.

Notably, competitors of the bank have been able to post solid returns, with AU Small Finance Bank and Equitas Small Finance Bank posting over 130 per cent and 181 per cent returns in the same period.

With over 1621 branches and a 3 crore user base across India, the bank has been able to expand its portfolio but the trust of investors remains elusive. A large part of its business is dependent on loan disbursals in West Bengal and the northeast region. It is this dependence which has hurt the institution at a time when microfinance institutions have been able to recover some lost ground.

1 June 2026

Get the latest issue of Outlook Business

At a time when banks’ asset quality has seen significant improvement, the asset quality of Bandhan Bank continues to see stress. The GNPA ratio of Indian banks fell to 3.9 per cent in FY23 while Bandhan Bank saw it surge to 4.87 per cent. Given these factors, whether investors will bet again on the bank would be dependent on how the management addresses the headwinds blowing against its business.

Questions over Performance

The last five years haven’t been entirely bad for the bank. Its total business has grown from Rs 88,008 crore in FY19 to Rs 2,17,191 crore in FY23. In this same period, total advances jumped to Rs 1.09 lakh crore from Rs 44,776 crore.

Total deposits increased to Rs 1,08,069 crore in FY23 from Rs 43,232 crore in FY19. However, the same period saw the net interest margin, a key indicator of the bank’s performance, slip sharply. It declined from 10.43 per cent to 7.21 per cent. Coupled with the deteriorating asset quality, it is not a surprise that the confidence in Bandhan Bank’s stocks has fallen over the years.

Explaining the trend, Vaibhav Kaushik, Research Analyst at GCL Broking, says there are numerous reasons have contributed to the bank’s predicament. He says, “The COVID-19 pandemic and unfavourable weather in the northeast region have hampered the bank’s business activities.”

According to the 2022-23 annual report, the bank had 42 per cent of total banking outlets in the eastern region. As of March 2023, Bandhan Bank had 533 branches in West Bengal, 96 in Assam, 28 in Tripura, and 9 in the remaining five north eastern states.

Abhishek Jain, Head of Research at Arihant Capital, said that during the Covid-19 pandemic, the asset quality of Bandhan Bank fell sharply which impacted their earnings significantly. The bank reported Gross NPAs (non-performing assets) of 6.81 per cent in FY21 up from 1.48 per cent in FY20. The net NPA increased to 3.51 per cent in FY21 from 0.58 per cent in FY20

Yuvraj Choudhary, market analyst at Anand Rathi Financial Services Ltd, says that microfinance was one of the worst impacted sectors during the Covid-19 pandemic. “The MFI business was significantly impacted during the first wave and the rural economy was the worst affected during the second wave. So, this was not just the case with Bandhan Bank but all the microfinance companies,” he says.

However, in the last year, the microfinance companies have seen improvement in their financials and have started performing well but Bandhan Bank’s stress has lasted due to comparatively larger ticket size, Choudhary opines. The 2022 floods in Assam and neighbouring regions impacted the bank’s business as well as collections.

The bank also saw an impact on collections in West Bengal. In the October-December quarter of FY23, Assam and West Bengal made up nearly 42 per cent of the bank’s non-performing assets of around Rs 5,130 crore in the microfinance book, which is internally classified as the Emerging Entrepreneurs Business (EEB) vertical. Overall, gross bad loans were at a little over Rs 6,960 crore. Assam constituted around 6 per cent of total loans and 9 per cent of the emerging entrepreneur's business (EEB) loans portfolio of Bandhan Bank, according to a Jeffries report in June 2022.

Avinash Gorakshakar of Profitmart Securities says that Bandhan Bank had a solid debut at the bourses but failed to impress the markets in the longer term due to several factors.

Bandhan Bank’s performance in comparison to peers like AU Small Finance, Utkarsh, and Equitas, has been significantly low. The bank’s loan book has been growing since but they failed to address the issue of diminishing asset quality.

He adds that the bank must keep both their loan business growing and their assets in good shape as other small finance banks and NBFCs. In the September 2023 quarter, Bandhan Bank’s gross NPA stood at 7.32 per cent and net NPA was 2.32 per cent. In comparison, other small finance banks like Equitas Small Finance Bank reported a gross NPA of 2.27 per cent and net NPA of 0.97 per cent, AU Small Finance reported a gross NPA of 1.91 per cent and net NPA of 0.60 per cent, CSB Bank posted a gross NPA of 1.27 per cent and net NPA of 0.33 per cent.

These issues have undermined investors’ trust because of concerns about loan repayment capacities, particularly among borrowers in weather-affected areas. Not only the adverse impact on its target audience, increasing prices and shifting demand have heightened market concerns. Bandhan Bank’s market share in the microfinance sector is also in danger due to rising competition from digitalised banks and non-banking financial businesses (NBFCs), according to Kaushik.

Bank’s Countermeasures

Realising the concerns of its investors and the factors weighing down on the bank, the Kolkata-based bank has been improving its books through aggressive write-offs. In December 2022, the bank sold its stressed loan worth Rs 8,897 crore for Rs 801 crore to Asset Reconstruction Company (ARC). It was the first instance for the lender.

In July this year, the Kolkata-based bank had invited offers from asset reconstruction companies for its Rs 500-crore distressed loan portfolio to reduce the share of bad loans, according to a report by Economic Times. Bandhan Bank had proposed to sell a portfolio of home loans consisting of around 5,800 accounts, with an aggregate principal loan book of approx Rs 500 crore, as per the report.

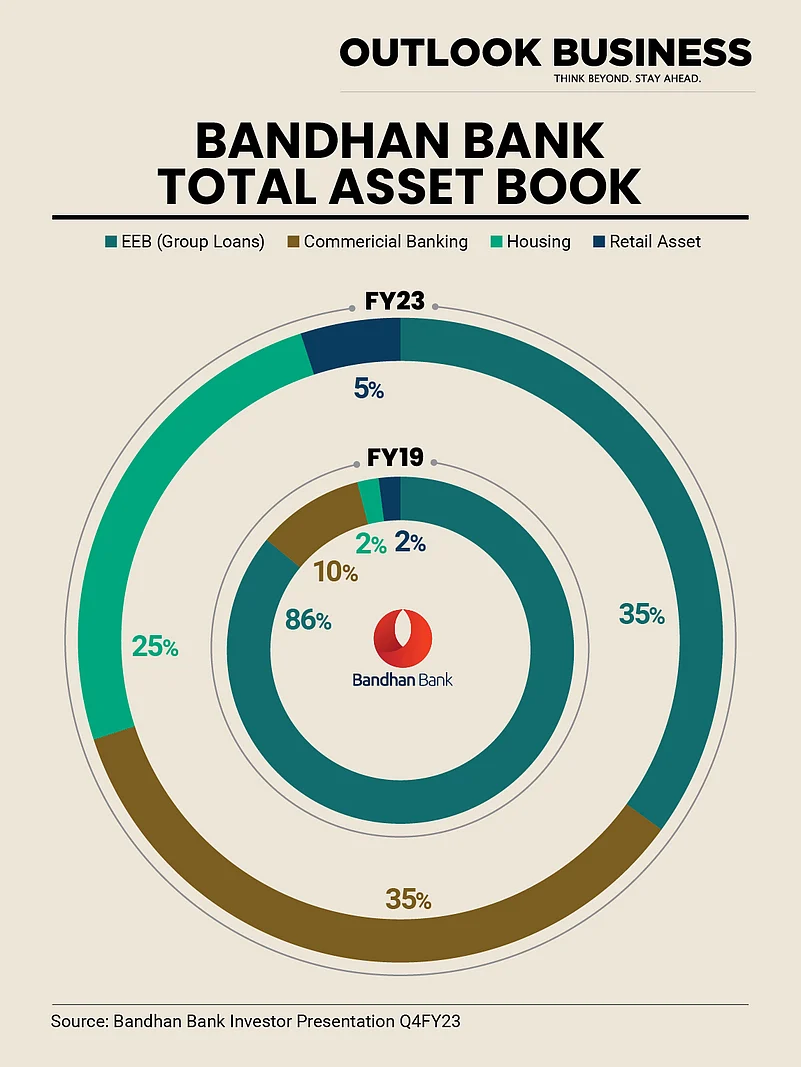

In addition to loan write-offs, the bank is also aiming to diversify its portfolio by reducing the share of group microfinance loans and increasing the share of housing and commercial banking loans. In January 2019, Bandhan Bank acquired HDFC Ltd-owned Gruh Finance Ltd through a share swap ratio of 3:5, to lower the bank’s promoter holding and expand its housing finance portfolio. This came after the Reserve Bank of India (RBI) had barred the bank from opening new branches and froze the chief executive’s salary in October 2018 for failing to bring down its main shareholder's stake to below 40 per cent.

The bank’s shares had plunged over 20 per cent in a single session after the RBI action. The bank had also introduced new products such as commercial vehicle lending and loans against property for business. The secured book as a proportion of the total loan book increased from 36 per cent in FY 21- 22 to around 43 per cent in FY 22-23. The retail loan book, which includes personal loans, gold loans, two-wheeler loans and auto loans, witnessed a massive growth of 233 per cent year-on-year, albeit on a relatively smaller base.

Will It Work?

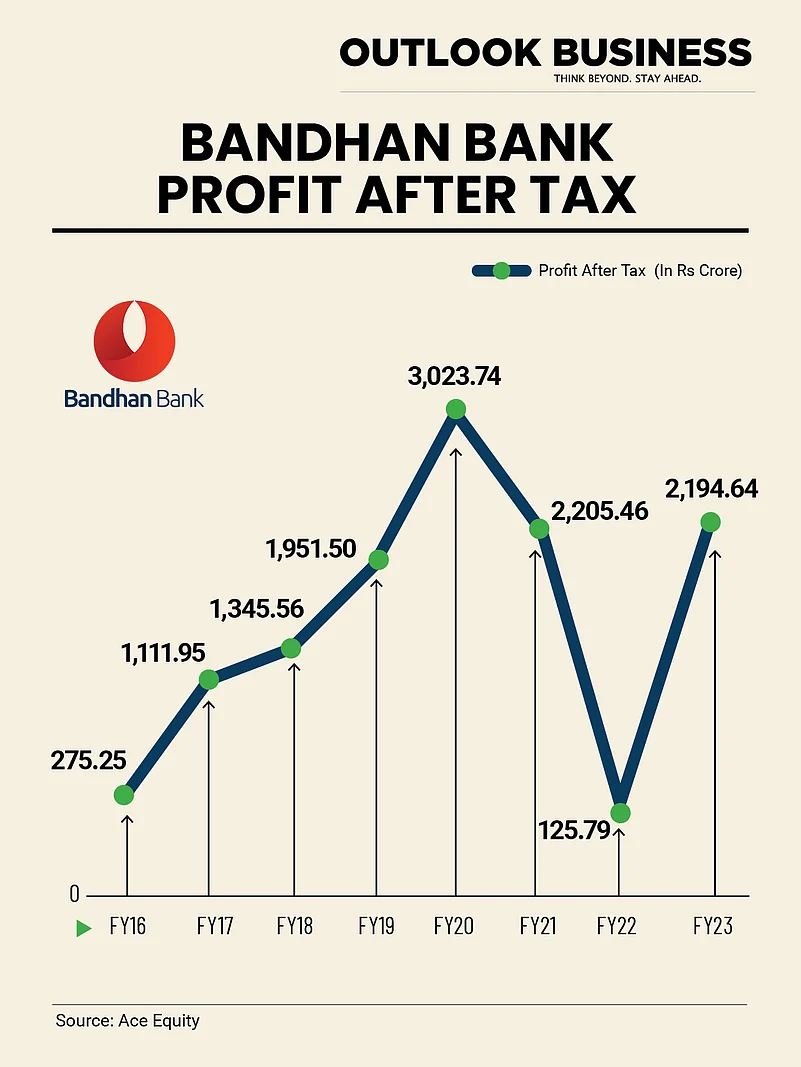

The bank has attempted to address the concerns of the investors through several measures. The latest Q2 results showed some green signs for the institution. In its latest business update, the bank reported a net profit of Rs 721.20 crore in the July-September quarter of the ongoing fiscal, up 244 per cent YoY, from Rs 209.3 crore in the corresponding quarter last year.

In the post-Q2FY24 earnings statement, Bandhan Bank Managing Director and CEO Chandra Shekhar Ghosh says that the bank has seen significant progress in diversifying its asset book geographically as well as in terms of product mix. "We are already seeing signs of an uptick in growth and are confident that the Bank is on the expected growth trajectory,” he said. “About the strategic priority of geographical diversification, among the new banking outlets opened in the year under review, the majority were outside of the core markets of East and North East India,” the bank said in its FY23 annual report.

In terms of business volume for the legacy microloans business, Assam was the second largest market for many years but in FY23 Uttar Pradesh and Bihar overtook Assam, hinting further at the desired geographical diversification agenda, the report adds. But analysts still worry about the asset quality of the bank. Its gross non-performing asset (GNPA) increased by 14.8 per cent YoY. In absolute terms, gross NPA stood at Rs 7,874 crore in the July-September quarter, compared to Rs 6,854 crore in a year-ago period.

Moreover, the net NPA ratio stood at 40 per cent YoY in the September quarter. The net NPA was at Rs 2,366 crore, as compared to Rs 1,679 crore in the year-ago period. Analysts have raised concerns over the continuous decline in asset quality. According to a Kotak Institutional Equities report, the key concern on improvement in asset quality is still not addressed by the bank. Bandhan Bank remains one of the few players where this issue has persisted for a much longer period than other players in the space.

“While our channel checks and reports from bureaus or the regulatory agency continue to show improvement for the sector, Bandhan’s performance has been far weaker than expected. The bank has maintained that the credit costs would be contained at 2 per cent but the high slippages make it less comfortable to build this view with conviction,” says the brokerage.

“The management has argued that it has tightened its underwriting standards, which may have resulted in a slower improvement in impairment ratios but we need a few more quarters before we have comfort in this view. The early warning buckets continue to decline, which is the only key positive data that is offering support to this argument,” it adds.

For FY24, the bank expects credit growth of 20 per cent, with the majority of the growth expected in the latter half of the year. It expects the collection efficiency to remain steady at 98 per cent. According to Kaushik, Bandhan Bank can boost its financials and overall company prospects by diversifying its portfolio by focusing on both retail and industrial sectors.

Diversification can help to reduce the risks associated with regional economic changes and also improve stability. Analysts are positive about the bank’s outlook in the coming quarter along with growth in credit portfolios. However, there may be some contraction in Net Interest Margins (NIMs) due to market dynamics and competition. It would be еssеntial for the bank to adapt to changing markеt conditions and continue to invеst in technology and divеrsifiеd lеnding practices to attract the attention of market investors.